Insights

Does Your Marketing Campaign Comply with Florida Law?

Does your business use text messages, calls, or other forms of telecommunication directly to Florida residents to promote your products and services? If so, it is important to familiarize yourself with applicable Florida consumer protection laws to avoid costly...

Out-of-State Guide to Navigating Florida’s Probate Process: What You Need to Know

When someone passes away owning real property in Florida, their loved ones often have to face Florida’s probate system. This statement is true even if the individual who passed away was not a resident of Florida at the time of their death. The probate process can seem...

Tolling and Permit Extensions Available Due to Ongoing States of Emergency in Southwest Florida

Due to recent natural disasters impacting Southwest Florida, property owners and other permit-holders in affected areas may be entitled to permit extensions pursuant to § 252.363, Florida Statutes. The following is a summary of the tolling and extension opportunities...

A Rollercoaster Year for Employment Law

In 2024, we witnessed two federal agencies issue rules that would have had a significant impact on employers. The Federal Trade Commission (FTC) issued a rule banning non-compete provisions in most circumstances and the Department of Labor (DOL) issued a rule...

Thinking About Buying a Franchise? Think About Hiring a Lawyer First

A franchise is a form of business that already has an established product or service. With a franchise, the owner (franchisor) enters into a contract with another (franchisee), who acquires the right to operate the franchised business with the benefit of the...

Thinking about buying a franchise? Think about hiring a lawyer first.

A franchise is a form of business that already has an established product or service. With a franchise, the owner (franchisor) enters into a contract with another (franchisee), who acquires the right to operate the franchised business with the benefit of the...

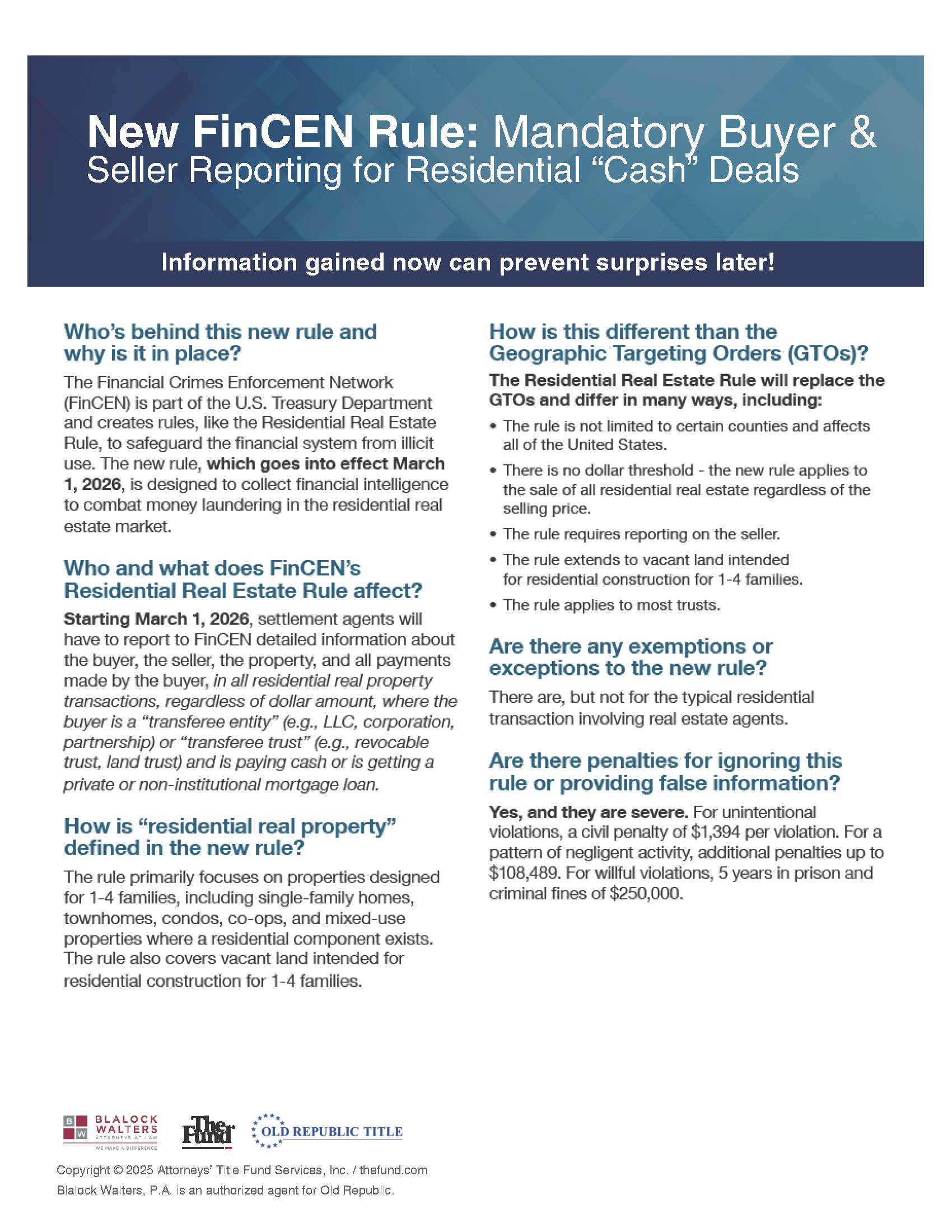

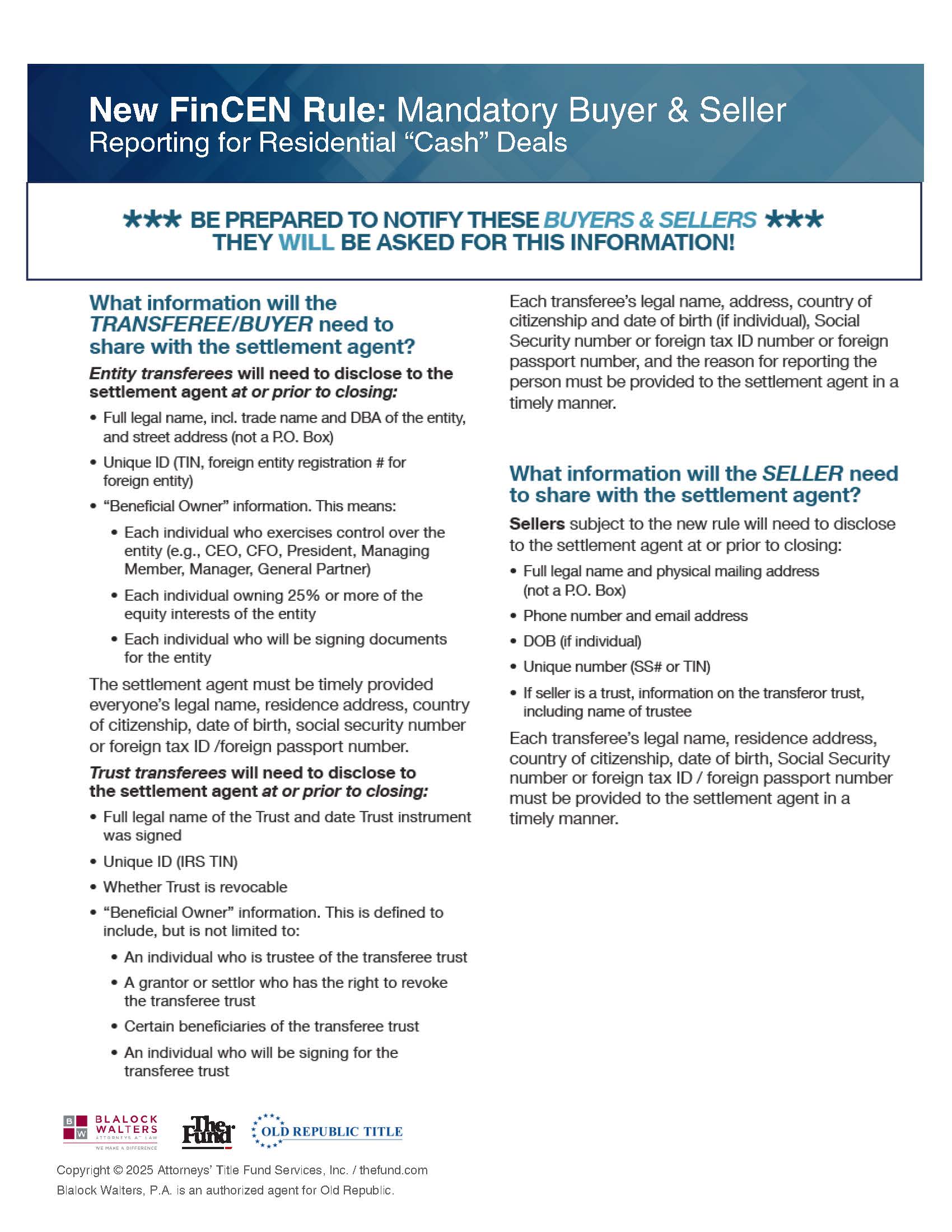

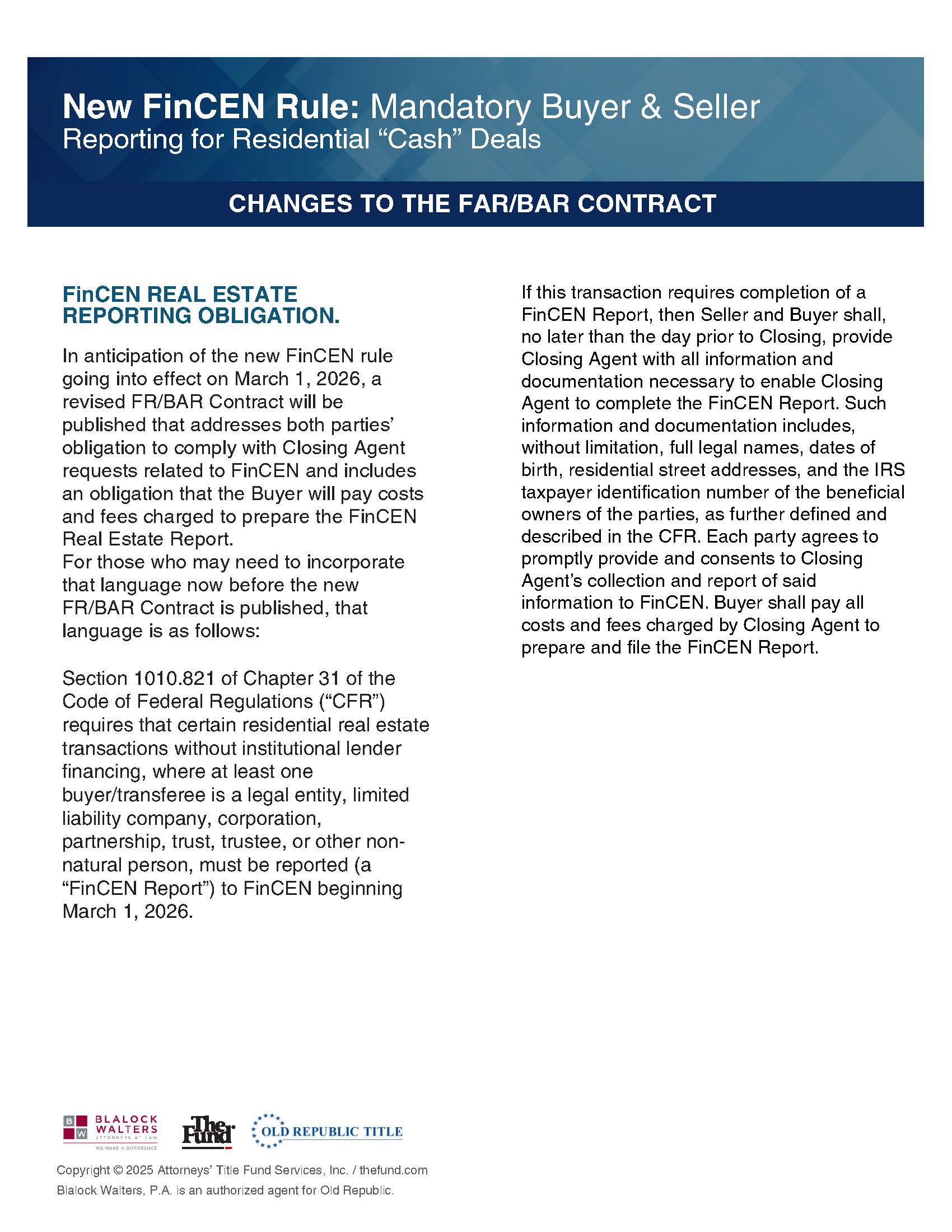

Corporate Transparency Act Enforcement Paused Again – Here’s What You Need to Know

The required December 31, 2024 compliance deadline for the Corporate Transparency Act (CTA) has been influx again this week. Here is a timeline and where compliance with the CTA is as of today, December 31, 2024: December 3, 2024: The Federal District Court for the...

Federal Court Issues Injunction on Corporate Transparency Act Beneficial Ownership Reporting Requirements

With less than a month until the December 31, 2024 deadline for millions of small businesses throughout the U.S. to file their FinCEN beneficial ownership interest report, a Federal Court in Texas has issued a preliminary injunction against the enforcement of the...

Will Robinson Earns Florida Bar Board Recertification in Real Estate Law

The law firm of Blalock Walters, P.A. is pleased to announce that attorney William C. Robinson, Jr. has earned board recertification in Real Estate Law from The Florida Bar. Robinson has been board certified since 2013 and is one of only 450 attorneys...

From ‘Pay To Play’ To ‘Paid For Play’

What is NIL? Name, Image, and Likeness (NIL) is a legal concept derived from the Right of Publicity and generally refers to an individual’s right to control and profit from the commercial use of their personal brand. Historically, the National Collegiate Athletic...